Most of the Indian’s mindset is insurance as investment instrument. Insurance is risk management tool and not an investment tool. In long term, insurance may give 2% – 3% effective returns to your money. You can never become rich by 2% – 3% returns from your money. Insurance and fixed deposits never make you rich. So come out of insurance trap and start investment.

Next to insurance mindset, the next investment mistake is looking for risk free returns. So people start investing on fixed deposits, Post office saving scheme, Senior citizen saving scheme, PPF and Sukanya samriddhi account. These investment gives fixed returns and but it is not worth in long term. Inflation makes all these investment are unworthy. People never consider inflation when they start their investment. To know the actual returns from investment, you have to measure with buying power of the money.

The buying power of money shows you actual returns.

Let us take an example milk price. In 2008, one litre milk is 15 rupees. 2020 it is 42 rupees. If you invested the 15 rupees in post office saving scheme for yearly interest 7%, it would become 35 rupees. But milk price is 42 rupees. So whatever money you deposited in post office scheme may look like investment, but it is not investment. I haven’t considered the TDS on this returns. If you consider the TDS, it would beome 32 rupees. Fixed deposit rates in post office is 7%.

2008 : 15 rupees invested => 32 rupees in 2020 in post office scheme

2008 : 15 rupees milk would be 42 rupees in 2020.

So how to get out of this trap. The only way to become rich is investing on hard assets. Assets like Gold, stocks, equity mutual funds or real estate. These investment has risk associated based on economy, market sentiment and demand. But these investments gives real returns and adjust based on inflation. Really you want to become rich, start investing in hard assets.

Not investing in risky investment is biggest risk in your financial plan.

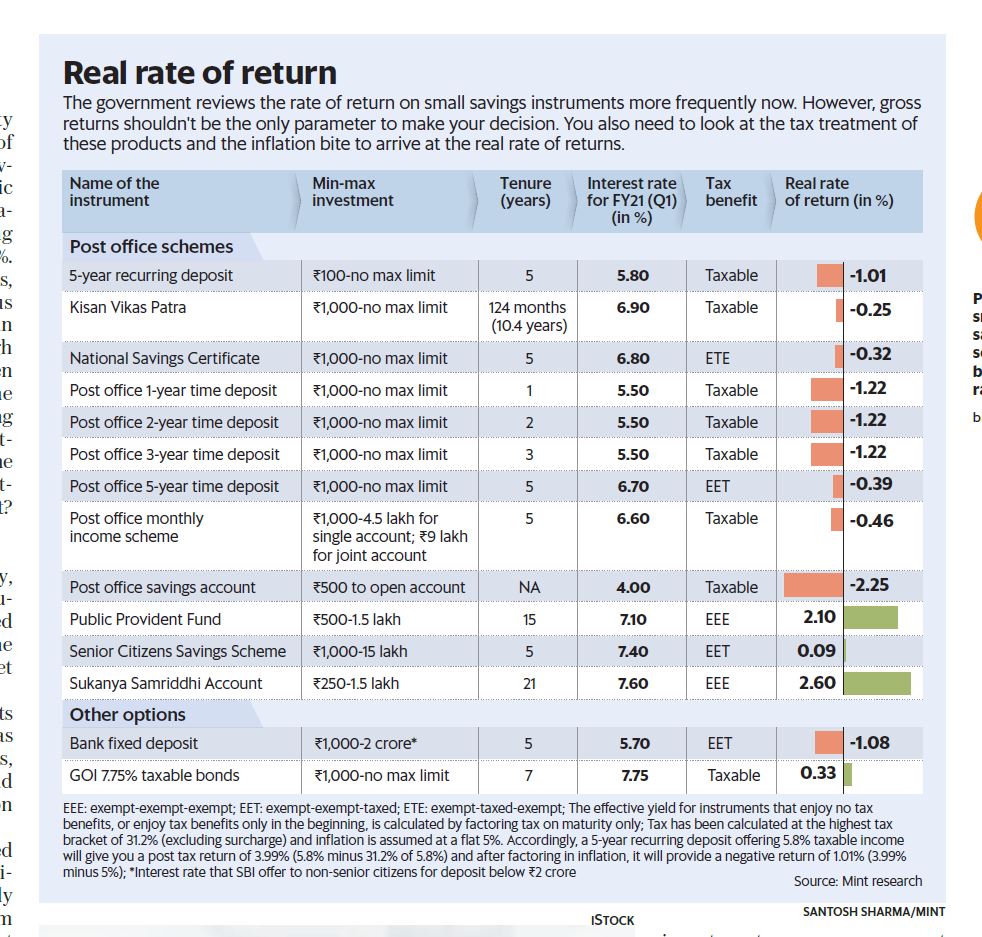

Yesterday “Mint” paper published an article to show real returns on these risk free investment. It is great article to understand the actual returns of PPF, fixed deposit, post office scheme and other saving investments. Thanks to mint for these valuable insights. Understand EEE in tax planning and investment returns.

So what is action plan to become rich. Select insurance policy and premium carefully. Your monthly premium should not exceed 5% of your monthly income. Maximum 5% in insurance. 15% of your investment in gold and remaining in equity mutual funds or stock market. In case you have confusion on selecting the best mutual funds to invest, start investing on Nifty index and Nifty junior index mutual funds.

5% on insurance

15% on Gold

15% on Nifty index mutual funds.

15% on Nifty Junior Index mutual funds.

Index mutual funds to start your investment.

You can start investing by selecting one Nifty index and Nifty Next or Nifty Junior mutual funds.

- UTI Nifty Index Growth Direct Plan

- HDFC Index Nifty 50 Growth Direct Plan

- ICICI Prudential Nifty Index Growth Direct Plan

- UTI Nifty Next 50 Index Growth Direct Plan

- ICICI Prudential Nifty Next 50 Index Growth Direct Plan

- DSP Equal Nifty 50 Growth Direct Plan

Change your investment from risk free investment to hard assets such as gold, stocks, mutual funds and real estate. Start proper planning and happy investing 🙂

SBI FD 5.7%, Inflation 4%. where to put retirement money after retirement.

Say”No” to Insurance. Get coverage of 1.35 crores instead of 27 lakhs.

Tax Planning – EEE = 100; ETE = 96; EET = 80; What is E and T ?

The one stupid financial mistake by indians. Never do that again