We in India think that “investing” in LIC is the mark of a genius and the teaching of parents. If LIC plans made you money, Indians would have been much richer by now. In contrast, LIC made Indian poorer. I could witness that people paid around 40% of their income as LIC policy premium thinking that it is best investment in india.

LIC never make you rich and it is not an investment

The best policy is not to buy any LIC policy. Why?

LIC agent would explain you the premium schedule and maturity amount. But he never consider the the inflation. LIC would give hardly 3% returns for your premium. But inflation is around 6% in India. You’ll get a premium burden of 20 to 30 years. You can’t get out of LIC premium once you started. You can stop an EMI but not an LIC premium.

If you miss the premium on time, you would be collected fine. How crazy is this !!

All the while, you’ll keep expecting “great returns” as the agent told you. And why not ? After all the nation is crazy about LIC plans. No matter what, at the end of the term with all the dreams of “jackpot maturity amount”, you’ll end up with 5% returns on your money, that is if you’re extremely lucky.

It would be too late to realize that all this while, the agents & LIC have made merry on your savings,in the name of “protecting your future & family”. Ironically, it is you who has been protecting and making them rich !!

Your LIC policy will make LIC and Agent Rich, not you.

If you are paying more than 20% of your monthly income as monthly premium to LIC, It is time to stop before it ruin your financial life. Many people consider LIC as tax savings, investment or protection of family. There is much better option for tax savings, Investment and family protection.

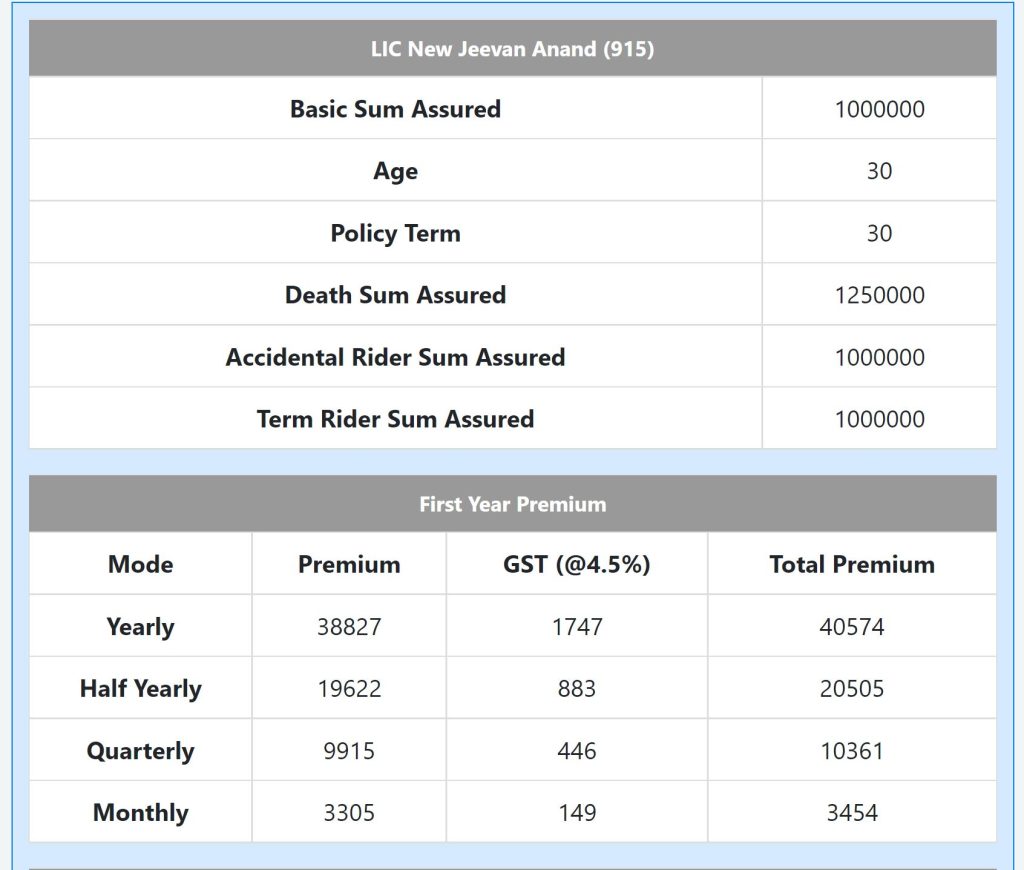

Let us explore LIC maturity calculator for Monthly premium of 3500 for 30 years. At the end of 30 years, you would get around 35 lakhs.

Tax saving option instead of LIC :

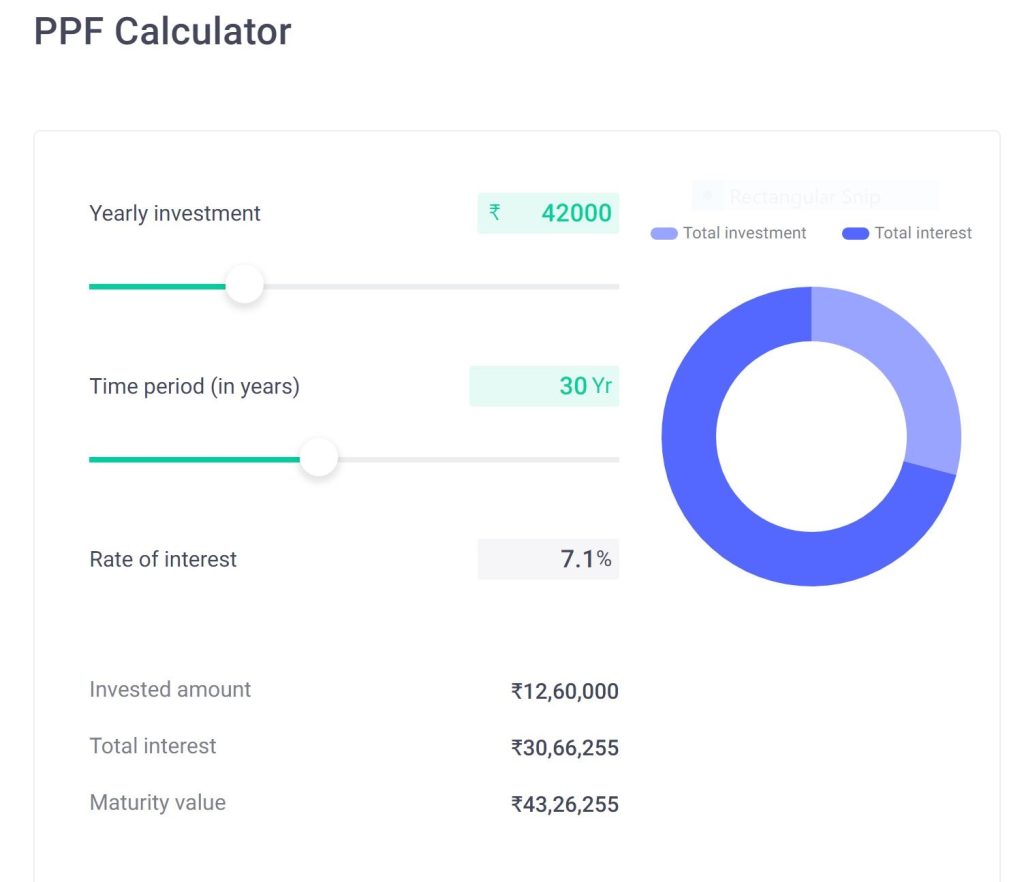

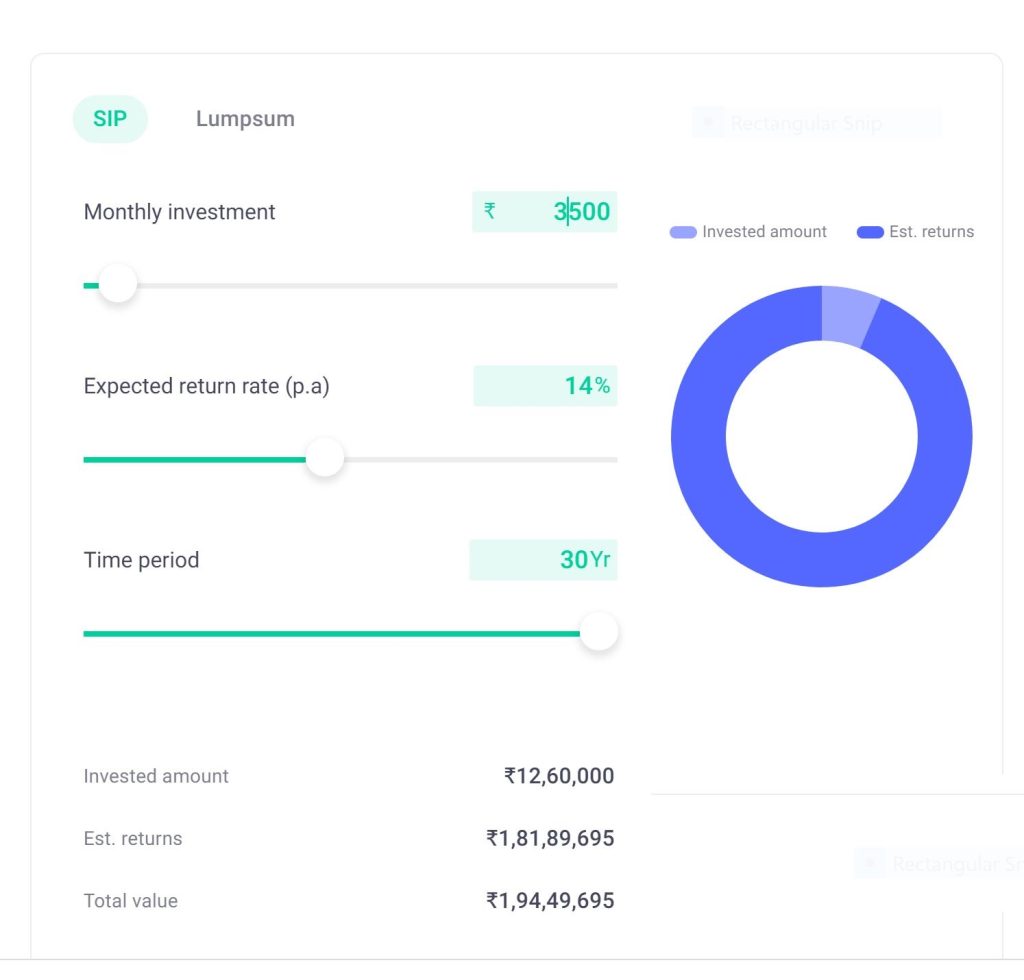

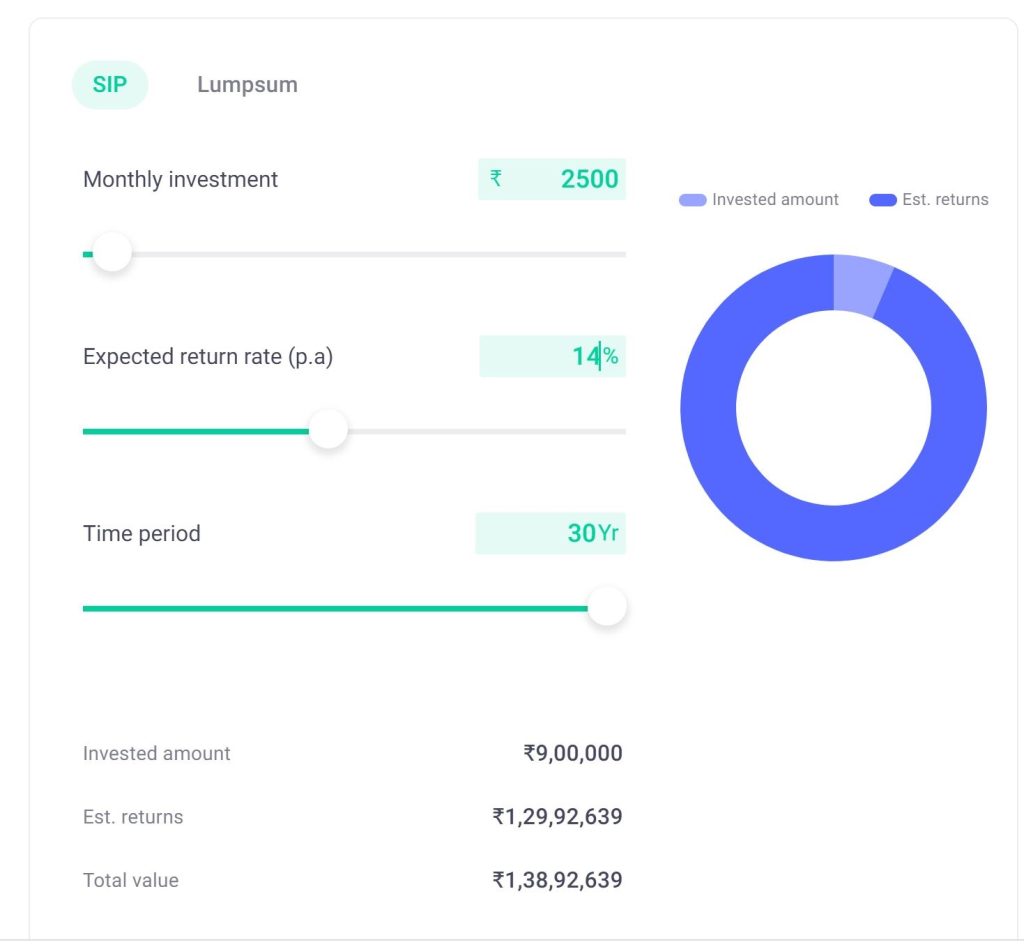

We can invest in PPF for 80C tax savings. PPF would give around 45 lakhs for 42000 rupees yearly premium for 30 years. We can invest in ELSS mutual funds. It would give 12%-15% returns in long term. You can invest in monthly SIP for 30 years. In long term, the same amount in SIP would give you 2.5 crores in 30 years. You can read more about data in 25 equity mutual fund schemes completed 25 years; offer around 17% average returns.

PPF and ELSS mutual funds investment can be claimed under section 80C tax saving option.

ELSS fund with 14% return in long term

Top ELSS mutual funds :

Investment option instead of LIC:

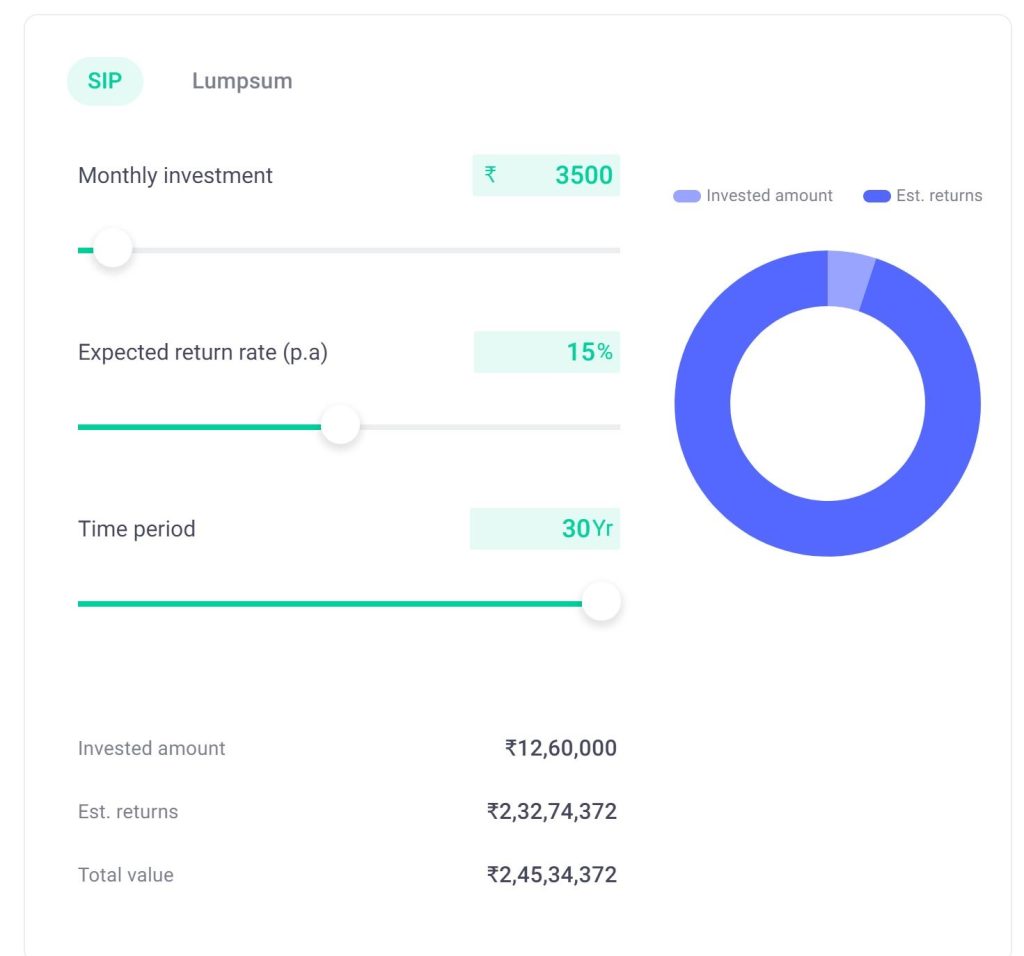

We can invest in Index mutual funds, blue-chip funds and large cap funds to get better returns with low volatility. In long term, It would give around 10% to 15% returns. Consider 15% interest, you would get 2 crores at the end of 30 years.

Top Blue-chip mutual funds :

- Nippon India Large Cap Fund

- Kotak Bluechip Fund Direct-Growth

- ICICI Prudential Bluechip Fund Direct-Growth

- IDFC Nifty 50 Index Direct Plan

Protection for family instead of LIC:

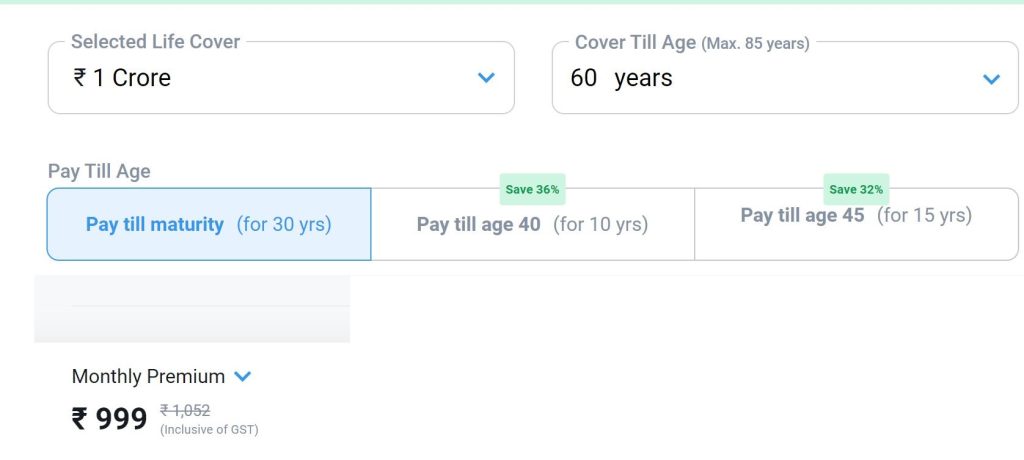

There are term insurance plan gives 1 crore to 2 crore coverage for monthly premium of 1000 rupees. Family would get lumpsum for survival and education expenses. Term insurance can be declared in 80C tax savings.

- ICICI Pru iProtect Smart

- Max Life Smart Secure Plus Plan.

- Tata AIA Life Insurance Sampoorna Raksha Supreme

- Aditya Birla Life Shield Plan

- PNB MetLife Mera Term Plan Plus

Protection for family + investment :

To get protection for family and investment, we can invest in 2500 in mutual funds and 1000 rupees premium for term insurance. So you would get 1 crore insurance coverage and you may get 1.5 crore after 30 years in mutual funds.

With 3500 rupees, 1 crore term insurance coverage + 1.5 crore wealth accumulation

Protection for family + Tax Savings + investment :

To get protection for family and investment, we can invest in 2500 in ELSS mutual funds and 1000 rupees premium for term insurance. So you would get 1 crore insurance coverage and you may get 1.5 crore after 30 years in ELSS mutual funds.

Both Term insurance and ELSS funds investment amount can be claimed in 80C.

Instead of LIC, there is lot of option in the Indian financial market. you can try different option to get better returns in the long term.